Fundamental Data Has Potential For Fireworks This Week

Following on from what was a reasonably quiet week last , expect heightened activity this week. Several key events could light the touch paper causing major moves on both Stock and currency markets.

As the week progresses the news begins to ramp up, the FOMC rate statement being the biggest fundamental event of the week. With equity markets moving higher and the dollar shaping out its next move possibly down, there will be keen interest in any signs of a tightening of monetary policy. While expectations are for rates to remain at 0.25%, QE3 will come into focus. Investors will be looking for any indication that this may be tapering off. Expect currency rates to change sharply if this is the case.

US rate decision is not the only think to look out for on Wednesday. The fast growing Chinese incoming releases monthly manufacturing figures which will give further indication as to whether the Chinese economy will be in for a soft or hard economic landing.

On the other side of the Atlantic we also have Bank Of England and ECB rate decisions due. While analysts have no prior expectation for any major changes to the currency interest rates (0.50%), it will be the press conference and accompanying minutes that will interest markets more. Clarification of monetary policy will be sought to provide longer term financial outlooks for each economy.

The week finishes with one of the most important sets of data on the economic calendar - the US Non Farm Payrolls. If markets have remained stable until this point of the week then expect the potential for volatility around this time. If the dollar has been hit earlier in the week then strong figures here could see losses reversed.

Key News This Week

In Focus

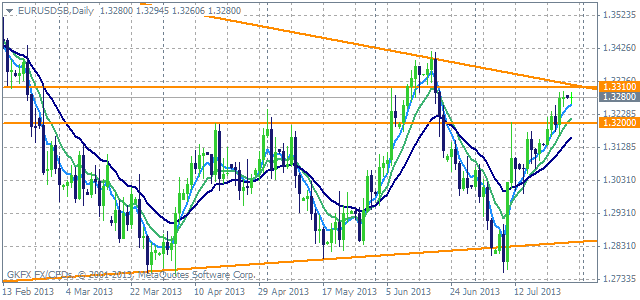

EUR/USD - The Euro is continuing to move higher and increasingly likely to pullback. Fundamental economic factors this week could provide this impetus. As the pair struggles to break 1.3300 this could prove a good level to go short.

Currency Majors

USD/JPY - The expected pullback in the pair has triggered, with price hitting the 50% retracement level at 97.70. We’d stay short for further falls back towards the 96.50 (61.8% of rise).

USD/CHF - In line with the rise in the EUR/USD, the pair has moved lower. 92.70 could prove to be the floor to the recent fall. The market looks bullish from here but it will depend upon this week’s fundamental data.

GBP/USD - The pair has struggled to add to recent gains and looks to be ‘topping out’. A break and close above 1.5400 could see further near term gains. However 1.5485 should provide the limit of any further push north. Remain bearish (but watch for Rate statement on Wednesday).

Major Indices

DOW - Follow an extended run of gains, events this week could see the market look to consolidate its gains. On a pullback expect 14,000 to provide a level of solid support. .

NASDAQ - 3300 proved to be strong support on the Nasdaq last week as expected. The bounce from prior identified support keeps the bullish stance alive. Look for further gains against his level this week.

FTSE - Staying above 6500 is supportive of further gains, with the recent pullback being viewed as corrective. Remain bullish or expect further pullbacks to be contained at the 5350-6400 level.

Commodities

Oil – Following strong gains last week, a pullback found support at the 106 which looks to be a temporary correction. Expect additional gains and a further push towards 110 over the course of the upcoming sessions.

Gold – Price remained contained by the $1340 level leaving the previous metal at a juncture. Watch for a break of this level to go long for further gains. A failure to post higher in the next few sessions is likely to see a resumption of falls back towards recent lows.

Stocks

Quite a few assets offered by binary option brokers are in focus this week, with action both sides of the pond.

Tuesday sees both data for release from UK stocks Barclays and BP, with Pfizer also looking to announce its Q2 profits. Also pay attention to British American Tobacco H1 figures due on Wednesday.

Later in the week we see further H1 figures due out from the likes of AstraZeneca, BAE Systems and Lloyds Banking Group. Across the pond it is the turn of the big oil majors Exxon and ConocoPhillips to report their Q2 profits. Exxon may provide the easiest play. If the recent clean up costs from the ruptured Pegasus pipeline are higher than originally anticipated, expect shareholders to start offloading more stock.

The finishes with H1 profits from the Royal Bank of Scotland Group.